| | It's About the Volatility, Stupid: How to Understand and Use SKEW

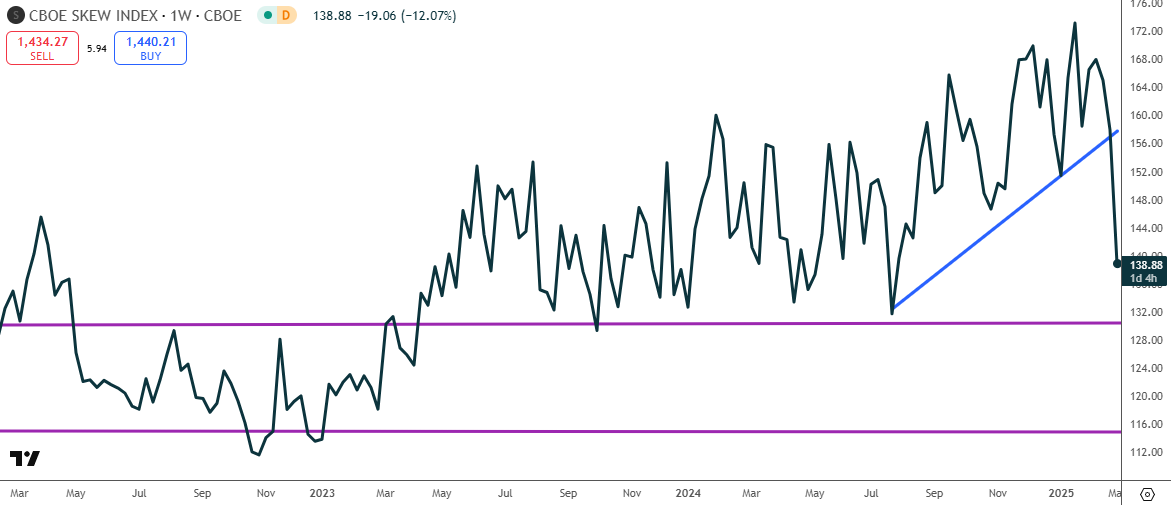

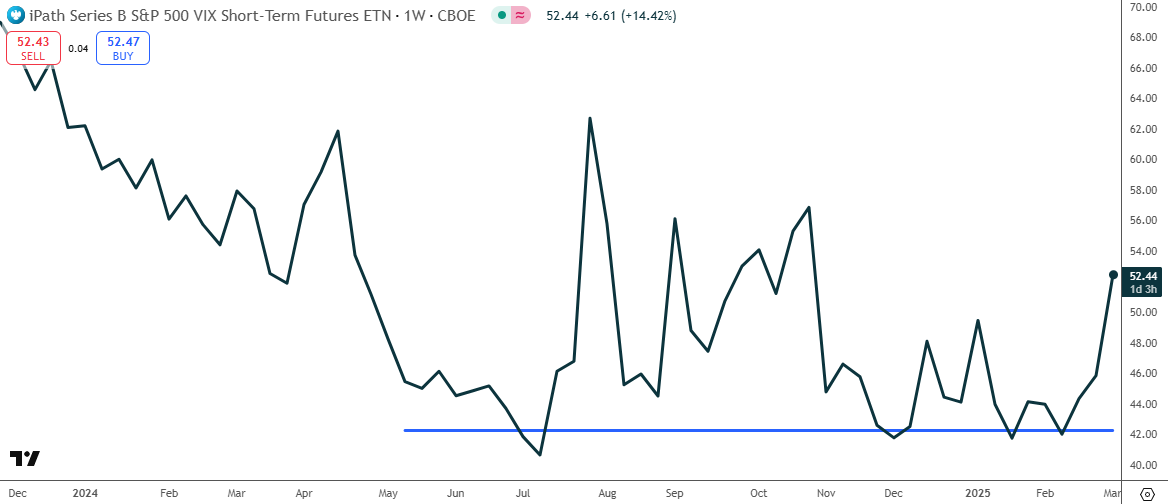

by Brandon Chapman, CMT | Market volatility can make us feel stupid at times. Just when you think you have it under control and you know what to expect… the rug pull happens! | As traders, that "rug pull moment" can be a big one - if we haven't managed our risk and had a plan to take profits. | Many times, the market catches a cold, and the average retail trader catches pneumonia. | Today, we're going to look to break that cycle and take control, no matter what gets thrown our way. | It starts with using this trusty tool… | Introducing the SKEW Index | While many analysts wonder what value the SKEW index brings, I find it hugely valuable. For those who don't know, SKEW, like VIX, is a measure of volatility in S&P 500 options. It functions as a good at-a-glance barometer of sentiment, like fear. | The issue SKEW-skeptics face is that they're looking to it for timing and that's not what it's about. All the index does is help you understand the degree the market is hedging. | I get it, you're probably looking at the VIX and saying that it was recently at 15 and that the players aren't hedging. | The trouble with that analysis is that it's not about whether they're hedging, but how they're hedging. | When the SKEW index is rising, the types of hedges that are put on cause the VIX to decline. Put very simply, they're buying puts and selling calls on the SPX. In fact, they generally sell more calls than puts, causing the average volatility to decline and the SPX implied volatility curve to further skew. These dynamics reflect that the crash risk is to the downside for the market generally. | | The negative skew picks up typically as these hedges are deployed and the market rises, causing the SKEW index to rise. The SKEW index typically falls as the VIX rises and more direct hedges (buying puts) are favored as equities are liquidated. | Applying SKEW Index | Historically, when the SKEW Index is over 130, you could interpret that as a high degree of hedging underway. One of the issues since 2014 is that hedging has been historically extreme. However, I still look at anything over 130 as high or extreme. Again, this isn't about timing, but there is a consequence of the type of expected volatility. The default position is to grind higher in the S&P as the risk expands significantly. | | I've been highlighting the pricing on 30-day and 90-day volatility as an indication of a near-term bottom in the S&P 500, but that's more about indicating that the VIX is at an extreme. Typically, as the VIX declines, the price of the SPX rises, but at times, the VIX doesn't really decline and remains stubbornly high. | It's at these times I look at SKEW to indicate whether we're poised to make a big upside move. In these circumstances, you really need to see SKEW normalize and move to the lower end of its historical range. That value is down in the 115 to 120 range. While the SKEW Index isn't there yet, it's sharply lower and could easily reach that level in the coming days. Low skew then cracks open the upside of the market with lower risk as hedges are drawn down and the VIX falls. | First Mover Option Pulse | We're looking for a first-mover advantage by identifying option pulses or prints that could impact the stock price. | Barclays iPath Series B S P 500 VIX Short Term Futures ETN Series B (VXX) | Today, there was a significant trade that was made on VXX. Normally, I'm not a fan of these products, but the trade is indicative of sentiment and money flow. Here is the big trade that was made today: | | These puts were bought quickly, and that's representative of a decline in the VIX, which generally points to a rise in the S&P 500. There were 10,000 contracts filled in a minute and is likely one trader who came in to buy them. | | | One thing about the VIX is that it always comes back to the mean and will eventually reach the lower end of its range. The difficulty is trading the pull back. Typically, I like the idea of selling put verticals on the SPY to benefit from implied volatility crush and a move higher in the index, but SKEW is still elevated, and pricing isn't there…YET! | If you're considering a trade like the one I highlighted, it's a very low probability trade with low risk and high reward. If the VIX comes down, expect the implied volatility of VXX options to similarly decline. Also, if the /VX futures can move out of backwardation quickly, it will help the trade as well. |

|

ليست هناك تعليقات:

إرسال تعليق