|

|

How to Survive the Market's "Return to Normalcy" (Most Won't)

by Brandon Chapman, CMT |

It's interesting to see traders' response to the current market environment. |

Some are pointing to how extreme the selling is, and pointing out the unfolding opportunity in hopping back into leveraged funds and averaging down. What most of these types of traders don't understand is that the past couple of years haven't been normal. |

The excess created by COVID-era monetary policy created an environment where junk was king. Negative cash flow? No problem! No real business? Even better! Blowing up on Reddit? Step right this way! |

If you were a meme, you were king… for a day. |

The one area that institutional investors piled into was the Magnificent Seven companies; COVID-driven policies and the resulting environment boosted the bottom lines of these companies. As we've discussed, the "dispersion trade" on Nvidia (NVDA) dominated the upside movement in 2024. Risk management was thrown aside as the FOMO trade was on! |

Of course, this type of movement isn't normal, and it all began to break down last summer, but retail investors didn't want to buy in. Post-election, retail began piling into stocks and margin debt began to expand greatly. President Trump was elected with a majority and mandate similar to President Harding's back in 1920. |

As strange as it may sound, any return to normalcy poses potentially significant risks for equities as we transition from a debt-based, FOMO-driven economy to a savings- and manufacturing-based one. Cold turkey, indeed… |

Here's how you can not only survive but grow your wealth during what comes next… |

Taking Stock of the Selling |

For traders who cut their teeth during the COVID market, the current selling may seem like the sky is falling. Yeah, we had a 20%-plus drop in 2022, but it was an aberration, and the last two years have been memory-holed. Even "older" traders who got their start in the wake of the Great Financial Crisis (GFC) may not understand the downside risks of a major credit event. As a result, they may think we're close to a bottom. |

I understand that it's always possible the market can bottom prematurely, and there is talk of a "Trump put." However, hopping back into meme stocks, crypto, and the like is a risky bet. Averaging down is even riskier as we have no idea how the massive credit expansion over the previous four years will play itself out. |

So, how bad is the current environment? It's got to be pretty bad, right? Well, let's look at some stats that shows the current position of S&P 500 and Nasdaq 100 stocks relative to their moving averages: |

S&P 500 Stocks |

42% above their five-day moving average 43% above their 20-day moving average 46% above their 50-day moving average 45% above their 100-day moving average 55% above their 200-day moving average

|

Nasdaq 100 Stocks |

30% above their five-day moving average 35% above their 20-day moving average 47% above their 50-day moving average 45% above their 100-day moving average 55% above their 200-day moving average

|

Let's contrast these percentages to December 18, 2024, or the March 2020 COVID sell-off and you'll see that we're not that extreme. Even the percentage of stocks above their five-day moving average suggests that near term bearish momentum isn't experiencing a lot of breadth at the moment. |

In other words, we're not at the point of maximum peril yet. |

The point of this analysis is that the capital rotation event I discussed in yesterday's newsletter is still in effect and the thought process needs to adapt to a more "normal" market environment. |

First Mover Option Pulse |

We're looking for a first-mover advantage by identifying option pulses or prints that could impact the stock price. Here are three that I thought were significant yesterday: |

Option Pulse No. 1: Occidental Petroleum Corp (OXY) |

The past couple weeks have seen bullish momentum build in the energy sector. That dynamic reversed yesterday as OPEC is looking to expand production in April. Cartels typically fail as positive pricing pressure begins to erode and the tendency is to cheat. The fact that they're looking to expand production is likely an indication that the cheating has already begun and the agreement to expand oil production is acknowledging that and the news definitely impacted stocks like OXY. |

|

The option pulse in the OXY puts was part of a generally bearish trading environment for energy producers yesterday. The oil futures market is still in backwardation, which is bullish, but near-term risks are to the downside if a recession is emerging and production increases. |

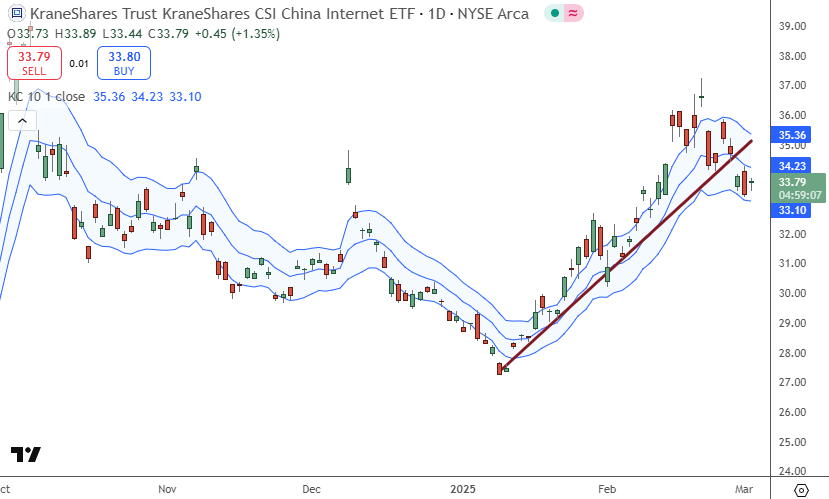

Option Pulse No. 2: Kraneshares China Internet ETF (KWEB) |

Yesterday was another recent first as bearish option pulses activity materialized in Chinese stocks as represented by KWEB. Last week I talked about the risks and the opportunities in China but warned about holding shares versus speculating using call spreads to capitalize on positive volatility skew in many of these stocks. The risk is a Chinese yuan devaluation that popped the Chinese stock bubble in October last year. |

|

KWEB broke its bullish trendline last Friday and had a bearish engulfing candle on Monday. The tide may be turning, and this may be a sign to have a plan to take profits in Chinese companies soon. The price is currently wading below the 10-day exponential moving average (EMA) is near the lower 10-day, 1 ATR Keltner Channel. |

|

One of the developments in the volatility of KWEB is the volatility skew has shifted. Previously, the OTM call IV was rising as you move out-of-the-money (OTM). Today, it's shifted more to the downside. That's an indication of some of the bullish speculation waning, but it also makes buying long put verticals cheaper. Here is a potential spread trade: |

|

The trade can be put on for around a $0.75 debit, with $75 total risk. That max gain is $1.25 or $125 per contract but consider taking profits at $1.28 for a 70% gain. |

ليست هناك تعليقات:

إرسال تعليق