Ticker Reports for March 4th

GitLab: Get In While It's Down—Big Rebound Ahead

GitLab’s (NASDAQ: GTLB) market may wallow near its early 2024 lows, but lower lows are unlikely, and a strong rebound lies ahead. The Q4 results and guidance for 2025 are the reason. However, the strong results and outlook weren’t the cause.

The market had set a high bar driven by ramping demand for AI software, which created a no-win situation for the stock price; no result short of a mind-boggling, NVIDIA (NASDAQ: NVDA)-like performance would have been sufficient to catalyze a rally.

The critical takeaway from the guidance is that this company forecasts another year of solid 20% growth, and the odds are high that the guidance is cautious. GitLab has outperformed every quarter since its IPO and is unlikely to break the streak due to increasing demand for AI products and services.

GitLab’s Strength Overshadowed by Market Forecasts

GitLab had a solid Q4, showing increasing demand and leverage with existing clients, which suggests the 2025 guidance is cautious. The company reported $211.4 million in net revenue for Q4, up nearly 30% and 250 basis points better than expected on an increased client count and deepening penetration. Clients contributing $5,000 in ARR grew by 15%, but the more prominent clients, contributing more significant $100K and $1M in annual ARR, grew by 29% and 28%, while retention came in at 123%.

Operating leverage is also growing. The company continues to post GAAP losses, but losses are narrowing, adjusted profitability is improving, and free cash flow conversion is impressive. The company widened its adjusted operating margin by 1000 basis points to 18%, generating $63.2 million in operating cash flow with a 98% free cash flow conversion. Free cash flow is up more than 150% yearly and is expected to grow in 2025.

The guidance is shy of the consensus reported by MarketBeat but no less potent. The company forecasted 23% revenue growth at the top line and is likely cautious given the strength of large client growth, penetration gains, and the 40% increase in RPO. Outperformance is the likely scenario; the question is how much.

The Analysts Affirm GitLab’s Moderate Buy Rating and Upside Potential

The analysts’ response to GitLab’s results and guidance is a mix of reduced and reiterated price targets that align with the consensus estimate. It is a 30% upside from critical support targets when reached. The takeaway from the commentary is that GitLab’s results weren’t all that impressive, but the demand outlook has stabilized, and the long-term forecasts are unchanged.

The long-term estimates include a 20% top-line compounded annual growth rate for at least the next eight years with a widening margin. Earnings are expected to grow at a rough 30% CAGR for the same period.

Institutional activity aligns with the outlook for higher share prices over time. Not only do the institutions own more than 95% of the stock, but their buying activity ramped to a multiyear high in Q1 2025. Institutional buying in Q1 hit a record high, more than doubled the selling pace, and netted a half-billion dollars worth of shares, about 6.5% of the market cap, with the stock trading near $58.

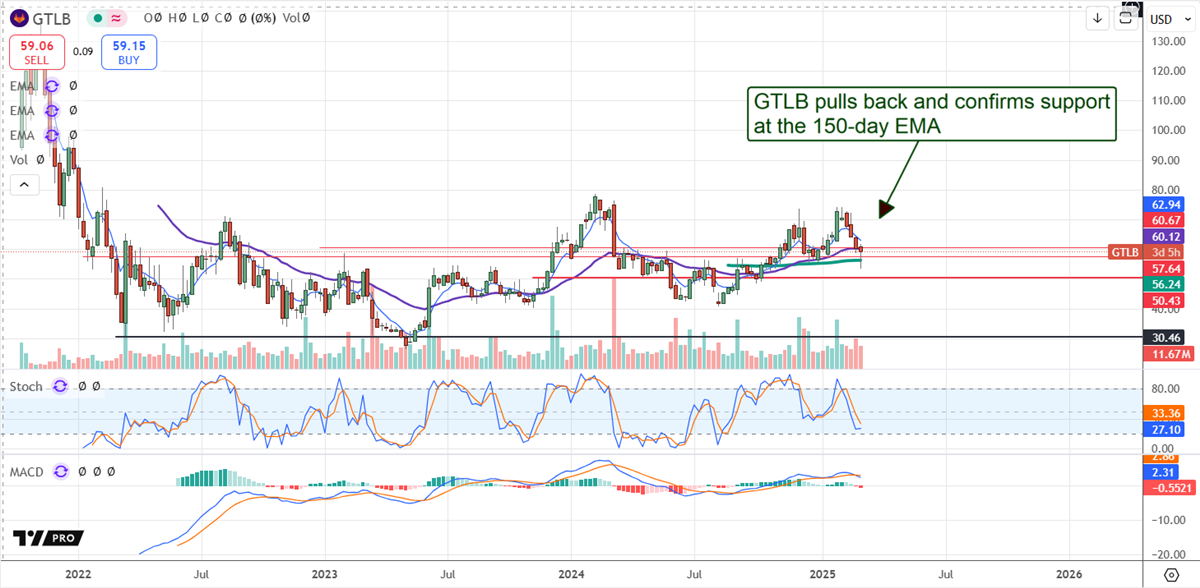

GitLab Confirms Support at a Critical Level; Sets Up for 2025 Rebound

GitLab’s price action fell the day before the release and opened with a gap following, but lower lows are unlikely. The market quickly rebounded from its early low to confirm support at the 150-day EMA, an indicator of long-term investor support, including institutions and analysts' followers. The likely scenario is that support will remain solid in the low to mid-$50s, causing this market to move sideways until traction is regained.

Trump's Fight Against The Biggest Act of Theft In Modern History

There's a Trump approved IRS-loophole which allows you to steer clear of government overreach and move your retirement savings into a private safe-haven, free of chaos and market manipulation.

Click Here For Your Free Copy

Rocket Lab's Plunge: Buy the Dip or Watch from the Sidelines?

Rocket Lab USA Inc. (NASDAQ: RKLB) has recently experienced a sharp drop from its 52-week highs, leaving current investors wondering whether this selloff presents a buying opportunity or signals more downside ahead. After a year of massive triple-digit gains, the stock's sudden reversal has sparked speculation about what comes next for this space industry contender.

Rocket Lab’s Meteoric Rise in 2024

Rocket Lab emerged as one of the most impressive performers in the aerospace and defense sector in 2024. The company gained immense popularity throughout the year, with its stock rocketing over 360% higher. As the space industry expanded and competition intensified, RKLB positioned itself as a legitimate challenger to giants like SpaceX.

The company achieved several milestones, including a record-breaking sixteen Electron rocket launches, a 60% increase from the prior year, and securing over $450 million in new contracts. All of this fueled a powerful rally, drawing the attention of both institutional and retail investors.

The Sudden Shift: Why Has RKLB Stock Plunged?

But as quickly as sentiment turned overwhelmingly positive, it reversed. As of Monday’s close, shares of RKLB have fallen 44% from their recent 52-week high in January. Given the volatility, this sharp selloff has many investors asking whether it’s time to buy the dip, lock in profits, or stay on the sidelines. To figure out the best move, it's crucial to unpack what's been driving this decline and examine the company’s latest earnings report.

Risk-Off Market Sentiment Pressures High-Growth Stocks

One of the most significant forces working against RKLB is the broader risk-off sentiment that has gripped the markets. Growing fears over tariffs, rising prices, and broader economic uncertainty have pressured high-growth, speculative stocks like Rocket Lab. As a company that’s still unprofitable, RKLB relies heavily on investor confidence, risk appetite, and flawless execution to sustain its lofty valuation.

Tariffs, for example, could disrupt supply chains and push costs higher, a tough blow for a company already reporting negative earnings, with Q4 2024 EPS coming in at negative $0.10, missing expectations of negative $0.09.

Neutron Rocket Delays Add to Investor Anxiety

This shifting market dynamic has been compounded by concerns over delays in Rocket Lab’s high-stakes Neutron rocket program. Initially set for a 2024 debut, the first launch has now been pushed back to the second half of 2025. Any additional delays could amplify the stock's downward pressure for investors, as missed timelines tend to rattle confidence in unprofitable companies banking on future breakthroughs.

Disappointing Q1 Guidance Fuels the Selloff

Rocket Lab’s recent earnings report didn’t do much to ease those concerns. The company announced a Q4 revenue of $132.39 million, a 59.3% year-over-year increase that narrowly beat analysts’ estimates of $130.57 million. But it was the guidance for Q1 2025 that stung.

Management expects revenue between $117 million and $123 million, well below Wall Street's forecast of $135.7 million. Adding to the disappointment, the company guided for an adjusted EBITDA loss of $33 million to $35 million, with a non-GAAP gross margin projected to land between 30% and 32%.

These soft numbers reinforced the broader risk-off narrative, accelerating the stock’s slide.

Is This a Buying Opportunity or a Warning Sign?

Yet, despite this, some analysts see the pullback as a chance to buy into Rocket Lab’s long-term story. Citi, for example, lowered its price target from $35 to $33 but kept a Buy rating. The firm acknowledged the Neutron rocket delay but noted that such setbacks are common in the space industry, viewing any near-term weakness as an “enhanced buying opportunity.”

Even with the recent volatility, Wall Street’s consensus remains cautiously optimistic. RKLB has a Moderate Buy rating and a consensus price target of $21.50, suggesting a potential upside of over 15% from its latest close.

Looking Ahead: A Long-Term Bet with Short-Term Risks

Ultimately, while the current market environment is challenging for unprofitable, high-growth companies like Rocket Lab, the long-term picture still holds promise. If the company can stay on track with its Neutron launch and keep building momentum in the space systems sector, this pullback might offer a compelling entry point for investors who believe in Rocket Lab’s future. At the same time, caution is key, given the stock’s sensitivity to market sentiment and the company’s lack of near-term profitability.

Collect $7k per month from Tesla's SECRET dividend

Tesla doesn't pay a traditional dividend....

But I just discovered a secret backdoor to collect a secret 69% dividend from Tesla…

Which could put up to $7,013 in your pocket every month…

Boeing Stock Is Edging Out Airbus Again, Here's How

The Boeing Co. (NYSE: BA) faced a lot of turbulence in 2024, from quality control issues, nightmare PR and the IAM union strike. The aerospace sector giant endured and resolved the union strike as the 33,000 striking mechanics returned to the assembly lines, bringing all systems back online in 2025. Although the company is still undergoing its 10% headcount reduction, the $500 billion backlog is more than enough to keep the company busy.

While Airbus SE (OTCMKTS: EADSY) took control of the oligopoly during the strikes, delivering more than double the number of aircraft at 766 than Boeing, it appears that Boeing is once again edging them out in its recovery.

Boeing Delivers More Planes Than Airbus in January

For January 2025, Boeing delivered 45 new aircraft versus 25 delivered by Airbus to 17 customers, according to Aerotime. Boeing delivered 30 aircraft in December 2024. It also marks the first time Boeing surpassed Airbus in plane deliveries since March of 2023. In January 2025, Boeing delivered 40 Boeing 737 MAX jets to customers including United Airlines Holdings Inc. (NASDAQ: UAL), Air Lease Co. (NYSE: AL) and Southwest Airlines Co. (NYSE: LUV), which exclusively flies only Boeing 737 MAX planes. This was the highest number of monthly aircraft deliveries since December of 2023 when they delivered 105 aircraft.

This was right before the fallout from the Alaska Air Group Inc. (NYSE: ALK) incident on Jan 5, 2024, when a defective door plug blew out of a Boeing 737 Max 9 airplane mid-flight. This incident started the cascade of incidents in 2024 and the FAA production cap of 38 MAX jets per month. Of the 40 737 MAX planes, 10 had been in storage. Boeing doesn’t expect to hit the cap until later in 2025.

Closing Out 2024 With a Final Kitchen Sink Quarter

On Jan 20, 2025, Boeing reported its fourth quarter of 2024 results, which were very ugly, but shares rallied afterward as the market viewed it as the last kitchen sink quarter for the company. The company reported a non-GAAP loss of $5.90 per share, which monumentally missed consensus analyst estimates for a loss of $3.22 per share. They missed estimates by $2.68.

Revenues sank 30.8% year-on-year (YoY) to $15.24 billion missing consensus estimates for $15.80 billion. The shortcomings were a result of the IAM work stoppage and agreement, charges for certain defense programs and costs associated with its layoffs. Operating cash flow was negative $3.5 billion, and free cash flow was negative $4.1 billion.

Segment Metrics Were Also a Kitchen Sink Disaster

For Q4 segment performance:

The Commercial Airplanes segment’s revenues fell 55% YoY to $4.76 billion with a negative 43.9% operating margin. By the end of the quarter, the 737 program resumed production as strikes were resolved at the beginning of November. The 787 program finished the year at a production rate of five planes per month with plans to expand its South Carolina operations. The Commercial Airplanes segment booked 204 net orders in the quarter, which included 100 of the 737-10 airplanes for Pegasus Airlines and 30 of the Boeing 787-9 plans for flydubai airlines. The segment also delivered 57 planes in the quarter, and the backlog was comprised of more than 5,500 plans valued at around $435 billion.

The Defense, Space and Security segment revenues fell 20% YoY to $5.41 billion, with a negative 41.9% operating margin. During the quarter, the company won a U.S. Air Force order for 15 KC-46A Tankers and secured an order for seven P-8A Poseidon aircraft from the U.S. Navy. The segment's backlog was $64 billion, and 29% of the orders came from customers outside the United States.

The Global Services segment's revenue rose 6% YoY to $5.12 billion, with a 19.5% operating margin driven by higher commercial volume and mix. The segment secured awards for the U.S. Air Force's F-15 Japan Super Interceptor upgrade services.

President Trump’s Made In America policies favor Boeing, with three of its manufacturing plants located in the United States. Boeing's Tianjin, China plant is a joint venture with Aviation Industry Corp. of China (AVIC) and makes aircraft for the Chinese market there. However, President Trump is levying another 10% on Chinese import tariffs in March, which may impact Boeing as it imports over 10,000 different aircraft parts from China.

MarketBeat Media, LLC dba TickerReport

345 N Reid Place, Suite 620, Sioux Falls, SD 57103.

No comments:

Post a Comment