The Latest Inflation Reports Are In… So, When Are Rate Cuts Coming? Dear Reader, Whether we’re shopping online, stocking up on school supplies at the local big box retailer, or filling up at the gas pump, one thing is clear. It seems like we’re feeling the pinch of inflation everywhere we go these days. That’s important to remember when we think about the market and the latest inflation reports. With each piece of data, we’re not just talking about a random statistic that can swing the market one way or another. We’re talking about real prices that affect people’s lives. I bring this up because Wall Street was laser-focused on two key inflation reports this week: the Producer Price Index (PPI), which came out on Tuesday morning, and the Consumer Price Index (CPI), which dropped on Wednesday morning. The market cheered yesterday’s PPI reading but was more ambivalent about the CPI report, though the S&P 500, Dow and NASDAQ are still up 3.7%, 2.7% and 5.1%, respectively, so far this week. Now, the reason Wall Street was keyed in on these reports is because investors want to know whether the Federal Reserve is gaining enough confidence to make key interest rate cuts sooner rather than later. So, in today’s Market 360, we’ll dig into the details of those inflation reports. We’ll also discuss how this impacts the Fed and what it means for the likelihood of rate cuts. I’ll also share how you should shift your focus in the meantime.

Producer Price Index Let’s start with Tuesday’s PPI report, which came in better than expected. The PPI rose 0.1% in July and is up 2.2% in the past 12 months. Economists were expecting a 0.2% increase in July. Core PPI, which excludes food, energy and trade margins, was up 0.3% in July, compared to forecasts of 0.2%. According to the Bureau of Labor Statistics, prices for final demand goods were up 0.6% and were the primary cause of the rise in July. Digging further into the details… - Energy rose 1.9% and accounted for nearly 60% of the increase in July.

- Gasoline prices increased 2.9% while electric power decreased 1.1% in July.

- Wholesale services fell 0.2% in July, marking the largest decrease since March 2023.

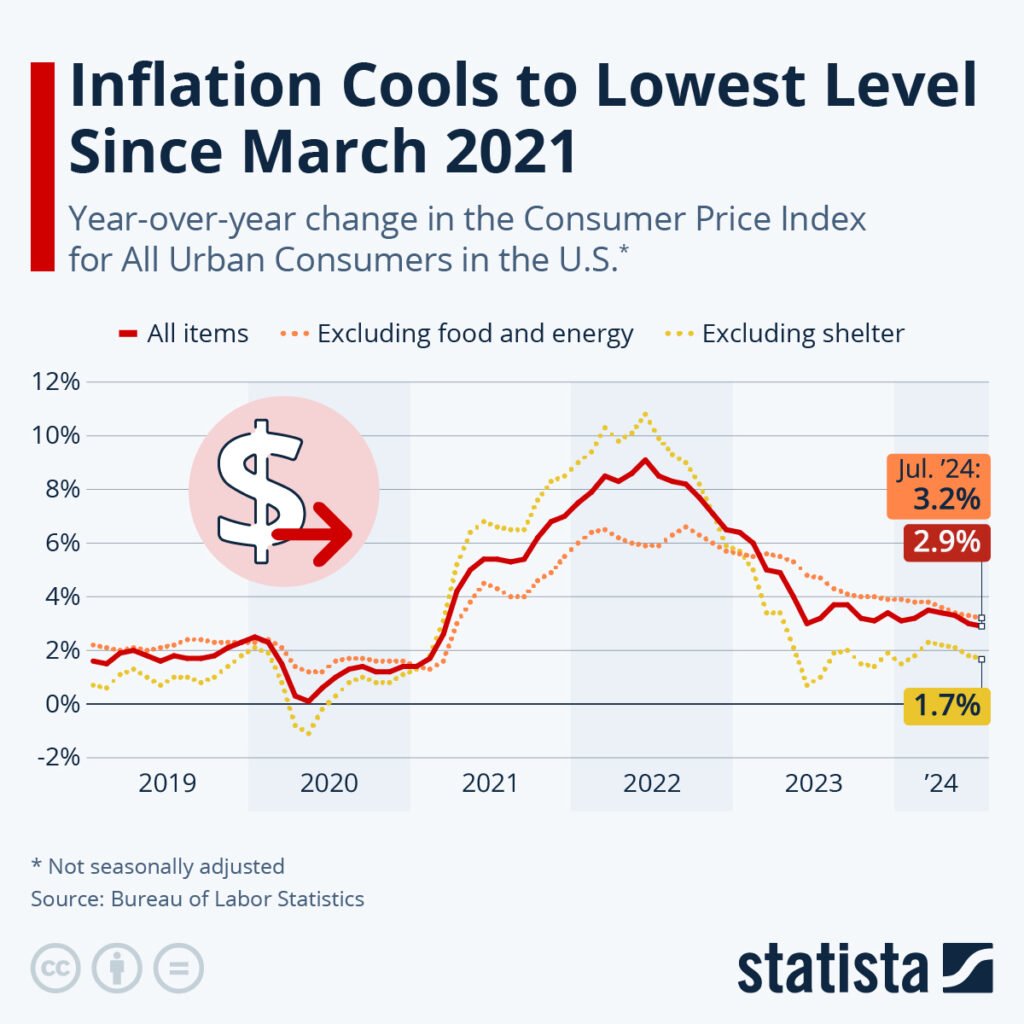

Consumer Price Index Yesterday’s CPI, which was in line with economists’ expectations, was a bit disappointing. The CPI rose 0.2% in July and is up 2.9% in the year, down from 3% in June. This was the lowest yearly increase in CPI since 2021. Core CPI, which excludes food and energy, rose 3.2% – the smallest 12-month increase since April 2021.  Looking deeper into the numbers… - The energy index remained unchanged in July, after decreasing 2.0% in June.

- The food index rose 0.2% for the month, the same as it did in June.

- The medical care index fell 0.2% in July, following a 0.2% rise in June.

- The motor vehicle index rose 1.2% for the month.

Most importantly, Owners’ Equivalent Rent (OER) rose 0.4% in July, up from a 0.3% increase in June. This is a problem. OER is responsible for 90% of the inflation in the CPI report. In other words, if housing costs could have come down more, then this CPI reading would be much lower. If you look around the country, you can see that prices are coming down in many places, but it’s just not showing up in the data yet, and that’s frustrating. When Is the Next Rate Cut? Now that we’ve reviewed the inflation data, the big question on investors’ minds is… When is the next rate cut? Next week, the Fed has its Jackson Hole meeting. Personally, I’d like to see a 0.5% rate cut before this meeting. The fact is we are seeing rising unemployment, declining inflation and plunging Treasury yields. I should also add that the U.S. retail sales came in 1% higher in July, while economists were expecting a 0.3% increase. So, that means we’ll likely see a 0.25% rate cut based at the next official meeting on September 18, based on yesterday’s CPI report and today’s U.S. retail sales report. Stay tuned for additional details on this morning’s retail sales report in tomorrow’s edition of Market 360. Now, I think it may be too little too late for the rate cut, but we’ll take it. It should provide a “turbo boost” to the U.S. economy. Where to Shift Your Focus In the meantime, the overall tone for the market has improved significantly since last week’s wild ride. First, this earnings announcement season has been stunning. So far, the earnings growth rate for the S&P 500 for the second quarter is 10.8%. That’s the highest growth rate since the fourth quarter of 2021. Second, the market has recovered from the pesky August air pocket experienced last Monday, August 5, when the market freaked out over the Japanese carry trade. (You can read more about what happened here.) And finally, market leadership hasn’t changed. That’s good news for investors who are loading their portfolio with fundamentally superior stocks, such as those included in my Growth Investor service. In fact, 63 of my Growth Investor recommendations have reported earnings so far and 47 of them have topped earnings estimates. The average earnings surprise is an impressive 25%. To break it down even further, I’ve had 20 companies post double-digit earnings surprises between 10% and 83%, and one achieved a 335% earnings surprise. Needless to say, my Growth Investor stocks are rallying strongly despite the broader market volatility. And while we wait for the next rate cut, there’s another event that could shock the markets again... The event is so big that I call it a financial tsunami. When this tidal wave makes landfall, its impact will be more violent and more severe than any financial crisis we’ve ever seen. But with every crisis comes an opportunity. And that’s why I’m preparing Growth Investor subscribers now for what’s coming. Because instead of getting caught up in the tide, we plan to ride the wave and profit immensely. Go here to learn more about the financial tsunami now. (Already a Growth Investor subscriber? Click here to log in to the members-only website.) Sincerely, | .png)

.png)

No comments:

Post a Comment