My Predictions for 2024 Dear Reader, “Hope smiles from the threshold of the year to come, whispering, ‘It will be happier.’”

The English poet Alfred Lord Tennyson clearly embraced each New Year with optimism, expecting it to be better than the last. And even though 2023 was an incredible year for the stock market overall, I happen to agree with Lord Tennyson. 2024 will be even better.

The fact is the stock market is poised to soar in the New Year.

In 2023, technology stocks led the overall market higher. The “Magnificent Seven” accounted for most of the S&P 500’s gain in the year’s first half. Although the market rally broadened in the second half of the year, it’s easy to surmise that tech stocks were the market leaders in 2023.

However, I don’t anticipate there will be one clear leader in 2024. The fact is the breadth and power of the stock market has improved dramatically over the past two months, with financials, industrials and real estate leading the market higher – not the Magnificent Seven. Small-cap stocks even staged an impressive rally since November, thanks to an “early January Effect.”

What this tells me is that the rally is real, and we’re going to have a much broader market in 2024.

Now, the rising tide will likely lift a lot of boats in the New Year. But I still anticipate fundamentally superior stocks will lead the overall market higher.

So, in today’s Market 360 , I’ll share my predictions for 2024. Then, I tell you where to find fundamentally superior stocks as we head into the new year.

So, what’s in store for the year ahead? Let’s take a look... 1. A More Accommodative Central Bank The Federal Reserve revealed a massive shift in policy for the New Year. Not only did the Fed leave key interest rates unchanged for the third straight month, but it also alluded to at least three rate cuts in 2024.

The Fed’s “dot plot” shows how the Fed expects three rate cuts in 2024 and another three to four rate cuts in 2025. That’s six to seven rate cuts over the next two years, bringing the fed funds rate to between 3.5% and 3.75%.

However, if the Fed wants to stay out of the political debate in a presidential election year – and trust me, it does – then there’s a strong likelihood the Fed could make all six to seven rate cuts before the election in November. 2. A Soft Economic Landing So, the Fed is doing the right thing by ending its tightening phase before it throws the U.S. economy into a recession. The fact is inflation has cooled dramatically this year. And even though it hasn’t yet reached the Fed’s 2% target, consumer prices are on track to reach this range no later than June 2024.

In a recent Wall Street Journal interview, Treasury Secretary Janet Yellen stated that she sees no reason “why inflation shouldn’t gradually decline to levels that are consistent with the Fed’s mandate and targets.” She also noted that the Fed has successfully engineered a “soft landing.”

I happen to agree with Yellen. The U.S. economy grew at a rapid 5.2% annual pace in the third quarter based on the latest estimates from the Commerce Department. And given that retail sales rose 0.3% in November, the Atlanta Fed recently upped its fourth-quarter GDP estimate. It now anticipates that the U.S. economy expanded at a 2.7% annual pace.

The deceleration from the third to the fourth quarter is primarily due to the big inventory build in the third quarter before the holiday shopping season. Falling energy prices and a dip in energy exports also contributed to slower GDP growth in the fourth quarter. However, inventories will rebuild at the start of the year, and energy prices will firm up as seasonal demand rises in the spring. So, first-quarter GDP growth will rebound. 3. Treasury Yields Continue Falling Treasury yields plunged after the Fed’s outlook for key interest rate cuts in the New Year. Yellen has also done a better job at managing Treasury auctions recently, which has allowed long-term Treasury yields to decline.

The 10-year Treasury yield peaked at 4.99% back on October 19 and was sitting around 4.25% prior to the Fed’s December meeting. Following the Fed statement and Fed Chair Jerome Powell’s comments, the 10-year Treasury yield dipped below 4.0% for the first time since late July. The 10-year Treasury yield now sits at about 3.89%.

In the wake of the plunge in Treasury yields, stocks exploded to the upside – and I expect this trend will persist as yields continue to moderate in January. 4. Election Year Bull Market 2024 is a presidential election year. Historically, presidential election years have been very positive for the stock market. According to Yardeni Research, the S&P 500 has climbed an average of 6.2% in presidential election years since 1932. The reality is that Republican and Democrat candidates alike run around promising everything and anything, and that tends to boost both consumer and investor confidence.

The 2024 election year will be particularly interesting, too. The candidates who recently won in Argentina and the Netherlands both have “big hair” and are fiercely independent. Specifically, Argentina’s new president, Javier Milei, is an economist and a libertarian. He wants to peg the Argentina peso to the U.S. dollar and slash government spending. In the Netherlands, the far-right Geert Wilders recently became the next Dutch Prime Minister.

Based on the theory that voters will continue to vote for “big hair” candidates, Gavin Newsom, Nikki Haley, Vivek Ramaswamy and Donald Trump all have the potential to be elected the next U.S. President. Interestingly, the winning candidate may not grab 50% of the vote since Robert F. Kennedy, Jr. is running as an independent. (By the way, I recently sat down with my friends at The Freeport Society, and they shared their prediction for who could be the next United States President. I urge you to watch that now.)

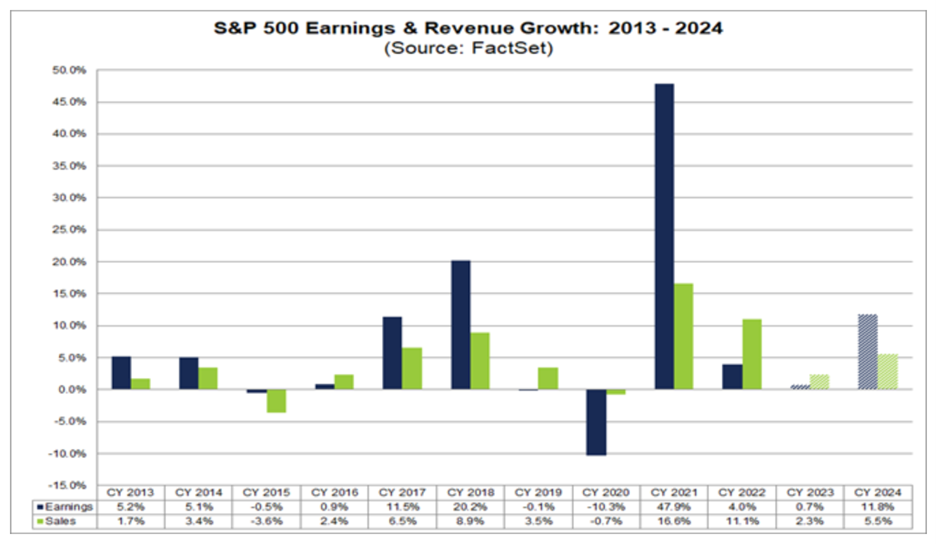

Overall, if history repeats, the stock market should rally right up to the November election, as endless campaign promises and multiple key interest rate cuts aid it. 5. Easier Year-Over-Year Comparisons And finally, the earnings environment is set to improve over the next several quarters, thanks in part to easier year-over-year comparisons.

According to FactSet, the S&P 500 should achieve 2.4% average earnings growth in the fourth quarter of 2023. For 2024, the S&P 500 is expected to report average earnings growth of 6.2% in the first quarter, 10.5% in the second quarter, 8.7% in the third quarter and 18.1% in the fourth quarter. Calendar year 2024 earnings are forecast to grow 11.5% year-over-year, compared to forecasted 0.6% average growth in calendar year 2023. |

.png)

.png)

No comments:

Post a Comment